You will have no doubt seen the recent media coverage regarding the Government’s proposed changes to probate fees. Despite widespread opposition, the Government has confirmed its plans to go ahead with these sometime in May 2017, although an exact date has yet to be announced.

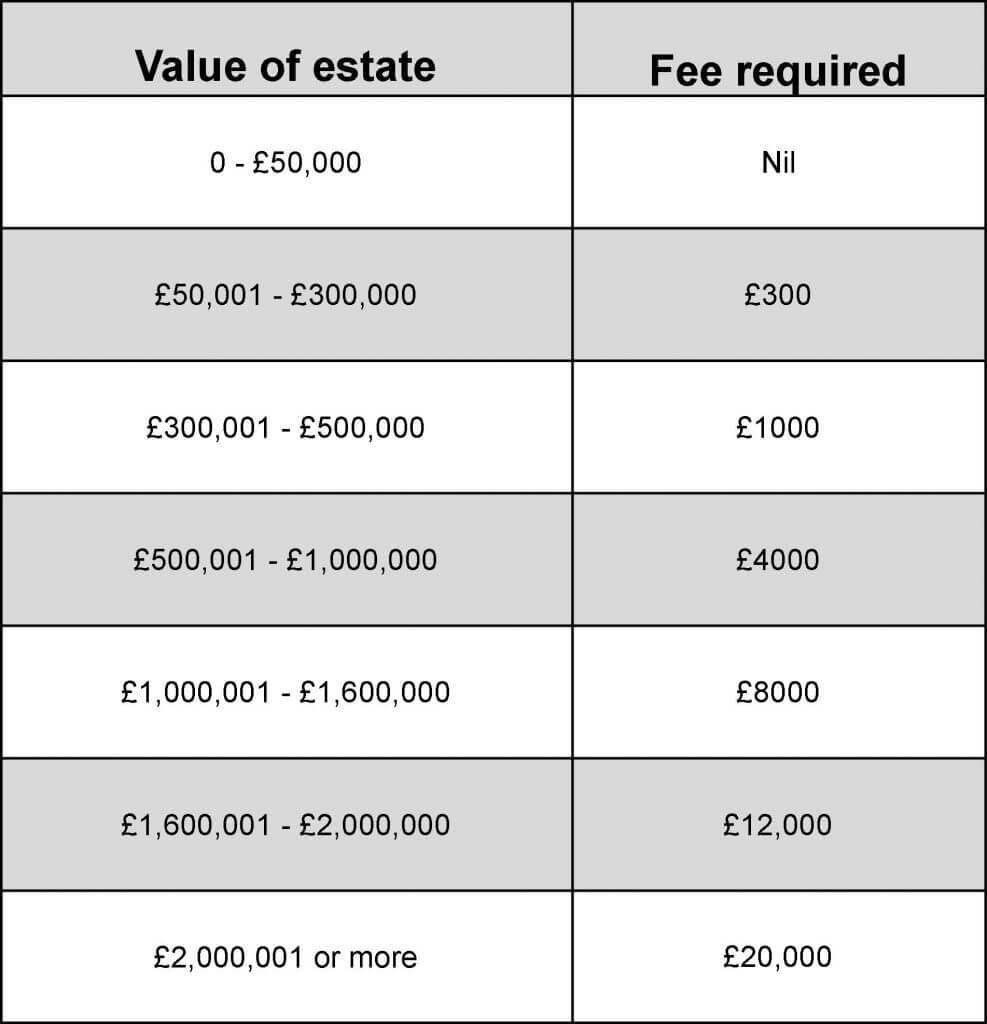

A Grant of Probate (or a Grant of Letters of Administration if there is no Will) must usually be obtained in order to release assets from a person’s estate when they die (for example, to sell or transfer their house or other assets to beneficiaries). Probate fees are currently set at a fixed level of £155 (if the Grant is obtained through a Solicitor) and £215 if obtained personally. The proposed new fees are set out in the table below:

Clearly these are vastly increased from the current fees and instead of being a relatively low fixed administrative fee, they are now linked to the value of a person’s estate. The Government is using these new fees to subsidise change in the rest of the court system, by raising an additional £250 million a year in order to improve and simplify the current Her Majesty’s Courts and Tribunals Service. The general consensus amongst legal practitioners and the public is that this is essentially a ‘back door’ death tax

Probate fees are paid ‘upfront’ before the grant is issued and Executors have access to the estate’s assets. While this is financially manageable at £155/£215, it becomes a consequential cost pressure for bigger estates especially where funds are tied up in assets and there is little actual cash. So, a primary concern is how the Executors of an estate will fund these fees. There are ongoing discussions within the banking industry about whether funds could be released from a deceased’s accounts pre-Grant, in order to fund the probate application. From these discussions it looks as if banks may agree this on a case-by–case basis. If there is little in the way of cash assets however, an Executor might have to take out a loan, or fund the payment from their own resources and subsequently claim this back from the estate once a Grant is obtained, which can take several months. In the case of an estate worth £2,000,000 or more (not unusual if the deceased owned property in the South East), an Executor will have to find £20,000 in order to apply for a Grant of Probate to administer the estate, which is no small sum.

There have been some suggestions in the media about how to avoid these upcoming fees. Asset reduction by lifetime giving or the increased use of trusts has been suggested, as has the joint ownership of assets. However these are not as simple a solution as they may appear. For example, looking at joint ownership, if assets are owned jointly as ‘tenants in common’, your share in that asset may be passed on when you die according to the terms of your Will. A Grant of Probate is then required to transfer or sell the asset in question. The other form of joint ownership (which is being advocated by the media), is as ‘joint tenants’. This means on death your share in that asset automatically passes to the surviving joint owner, regardless of the terms of your Will. With this type of ownership, no Grant of Probate is required.

Whilst it may be possible to own some assets as joint tenants, such as your main home and other real estate or bank accounts, most other assets can’t be owned jointly (securities, ISAs, bonds etc). A Grant of Probate will therefore still be required in order to transfer or sell these assets and the proposed new probate fees will still be payable, even though your home and bank accounts are owned as joint tenants. It is also important to bear in mind that owning assets as joint tenants which pass automatically by survivorship to your co-owner means you have no control over who will ultimately inherit that asset. Both ‘solutions’ ultimately reduce a person’s choice over the destination of their estate.

Assuming the introduction of these fees remains legally unchallenged, these will become as much of a consideration as other Estate planning concerns, such as inheritance tax. Strategies to reduce and fund these costs must be considered as part of an overall careful Estate planning strategy, to ensure the people you wish to inherit do actually benefit, and which also incorporates proper inheritance tax planning.

In the meantime, there is currently a petition for a review or cancellation of the proposals organised by the Law Society which we encourage everyone to sign: https://petition.parliament.uk/petitions/188175

The Private Client team at Teacher Stern is here to assist Executors who need to apply for a grant or wish to discuss whether one is needed, and those who wish to make or reconsider their Wills in light of these proposals.

Contact:

Elizabeth Jones, Partner & Head of Private Client or Nicola Edmondson, Senior Associate